Yesterday, a friend of mine texted me the following: “Not that anyone knows. Do you think we will retest the lows or its upwards from here?” That seems to be the $64K Question these days, doesn’t it? My response was pretty simple: “With the Fed and the Feds throwing crazy money at the situation, who knows? But for all this cash sloshing about, yes, we would easily retest the lows…and probably then some. However, 16.8 million have filed for unemployment over the last 3 weeks, and nobody seems to care. We are waiting to see what earnings season looks like, because trying to value the markets right now is almost a fool’s errand.”

Yep, that about sums it up.

Make no mistake about it, in this week’s battle between liquidity and bad economic data, liquidity won. Better put, the promise of liquidity won, because whether the funny money from the Treasury and the Federal Reserve’s open checkbook will have the desired impact is still a question mark. Certainly, it is inconceivable to imagine they wouldn’t have a positive short-term impact on economic growth. Some jobs that would have otherwise been lost won’t be. Some businesses that would have closed their doors forever might not. All of it, but will it be enough? And will it get to where it needs to be in time? Because many of the intended beneficiaries of this largesse are dealing in minutes, hours, and maybe a day or two…not weeks, let alone months.

Then, what is the old expression? The devil is in the details? Well, that is doubly true here. Consider this: in order to get this relief/stimulus money you have to go through a qualified intermediary, namely a bank. There are strings to the money, a bunch of them that need attestation, and the bank still has to underwrite the credit (to some degree). Why? Well, because it really doesn’t want to holding a whole bunch of low interest rate, poor credit loans if something goes amiss.

Further, it isn’t too hard to imagine a lot of this money being thrown around to protect jobs might not actually do that. What would stop some borrower from taking the money at a low interest rate, and then laying people off? Even worse, realizing their business is a lost cause and closing up shop? SBA won’t forgive the loan in that scenario, and Bank ABC is stuck tracking the borrower down to get its money back. That is why banks are primarily processing existing clients, preferably those they have already underwritten, and sending others (strangers) packing.

Seemingly shifting gears, have you ever been to a restaurant and the portion size of what you ordered is so massive it seems like you aren’t making a dent in the thing? That no matter how much you eat there is still enough for a family of 4 on the plate? That is how I feel when I think about the details, the potential for error, and the unintended consequences of these programs. Again, they WILL mitigate the downside to a still undetermined degree. It was probably necessary. However, I would be willing to bet you a beer, when all is said and done, we will wonder just where all the damn money went. Even more, we will wonder just how in the hell THEY (pick your favorite undeserving individual or entity) got ALL of THAT?

This morning, I drove my daughter out to the oral surgeon in Trussville, AL, to finally get her wisdom teeth pulled. Whether what I observed was all COVID-19 related or not, I don’t know. However, there were many more empty, and I mean truly empty…signs taken down and parking lots roped off, former restaurants and stores on Highway 11 than the last time I was on that stretch of road about 3-4 weeks ago.

Perhaps people who live in that area of town can tell me I am wrong.

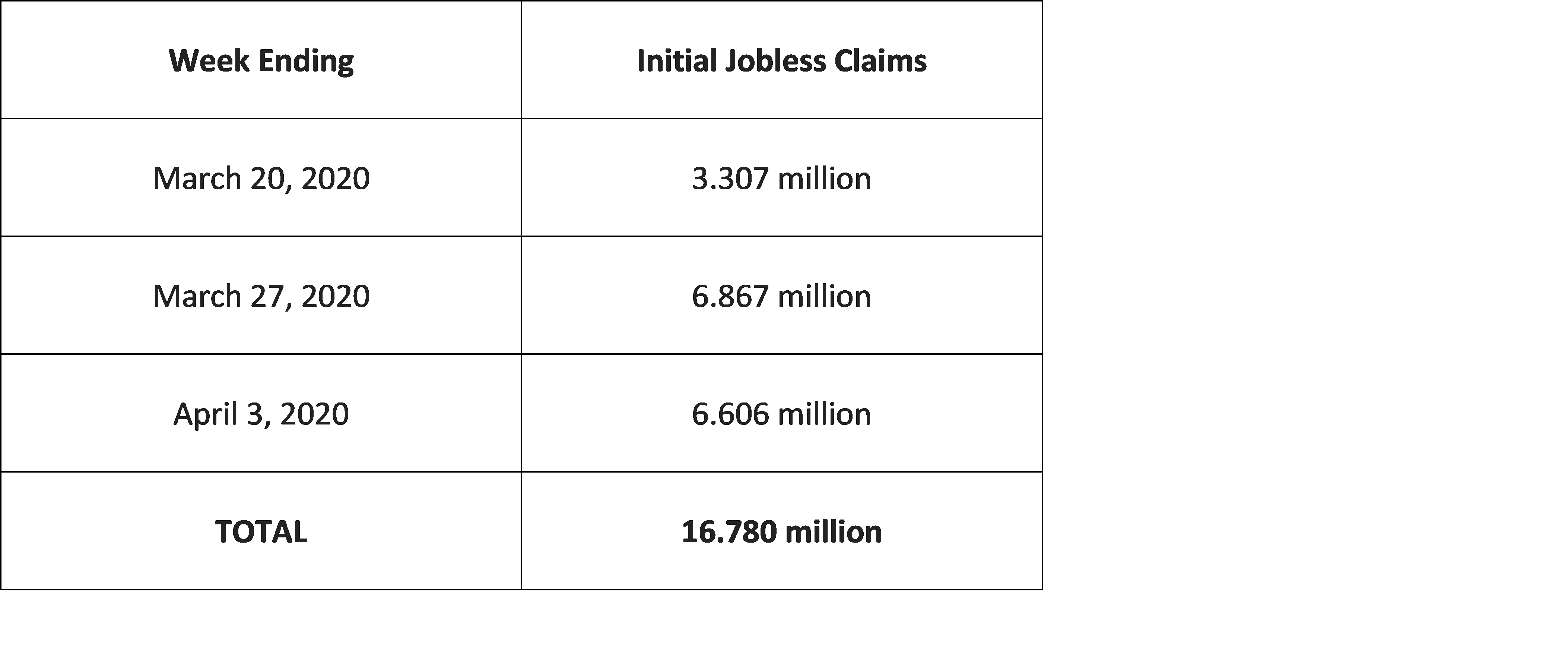

However, what I saw would go hand in hand with what I have been reading, and what you have undoubtedly also been reading. Millions of jobs lost, businesses closing, and all of that. The true economic data has been distressing. Consider the following:

To put that number into perspective, consider there are about 162.913 million people actively participating in the US workforce according the BLS Household Survey. If ALL of those people remain unemployed and if the size of the workforce remains constant, the Unemployment Rate has spiked up to about 14.7% over the last 3 weeks. To put THAT number into perspective, the highest Unemployment Rate in the United States since January 1948 (which is as far back as the Bloomberg goes) has been a 10.8% in November 1982 until April 2020.

To put that number into perspective, consider there are about 162.913 million people actively participating in the US workforce according the BLS Household Survey. If ALL of those people remain unemployed and if the size of the workforce remains constant, the Unemployment Rate has spiked up to about 14.7% over the last 3 weeks. To put THAT number into perspective, the highest Unemployment Rate in the United States since January 1948 (which is as far back as the Bloomberg goes) has been a 10.8% in November 1982 until April 2020.

Meanwhile, since the end of February, as the US economy slowed to a crawl in March, the S&P 500, arguably a gauge on the health of the US economy and corporate America, is down about 5.3%…total return since the end of February. While terribly good, it is, um, a lot better than the economic data would suggest it should be. The reason, if I need to ask? Liquidity or the promise of liquidity. We all know it.

Hey, man, it feels good…great even. Whew. The powers that be aren’t going to let us march off into the economic abyss! Praise be, for now. You see, I imagine at some point, in the not so distant future, people will start to notice the economic data and pay attention to earnings a little more than they have recently. Then they/we will have to start putting a more realistic valuation on the market(s).

Shoot, you know, the way investors acted this week, you would have thought they were expecting the Easter Bunny or something.

I hope this finds you and your family safe and as happy as you can be.

John Norris

Chief Economist

As always, nothing in this newsletter should be considered or otherwise construed as an offer to buy or sell investment services or securities of any type. Any individual action you might take from reading this newsletter is at your own risk. My opinion, as those of our investment committee, are subject to change without notice. Finally, the opinions expressed herein are not necessarily those of the reset of the associates and/or shareholders of Oakworth Capital Bank or the official position of the company itself.